ISSUES IN CAPITAL MARKET ECONOMICS

Spring 2015

ECON 400/400G

ISSUES IN CAPITAL MARKET ECONOMICS

Spring 2015

External Sites:

Federal Reserve Info:

Federal Reserve System Article Search Engine / FRB of New York / FRB of St. Louis / Index of SEC Rules /

Blogs/Discussions/Research

Fama-French Forum/ John Cochrane CGSB Site/ Xavier Gabaix NYU Site/ Streetwise Professor/

Current Data

Bloomberg Economagic Economic-Financial Data

Dr. Brian Goff

GH 414/745-3855

Office Hours for Spring 2015: MW 9:30-11:30 (appointments & drop-ins welcome other times)

Objective

To acquaint students with several current issues on the border between

macroeconomics and financial economics, financial market microstructure,

and financial market regulation

Resources

Selected Readings On-Line

Grading (Undergrad)

Exam

I

= 30%

Exam II

= 30%

Assignments

=

20%

Reading Quizzes

=

10%

Total

=

100%

(A=90-100; B= 80-89; C= 70-79; D = 60-69; F < 60)

Weekly Reading Quizzes: Short, multiple choice quizzes over readings

Empirical Assignments/Presentations: On the empirical

assignments, students should put together a short (5-10 minute)

powerpoint presentation summarizing the empirical work. The

powerpoint slides should be

printed and turned in. The aim of the presentation is to summarize

the material (or the most important parts of it) in ways that best

communicate it to the other students using cut/past graphics, data,

bullets. Remember, more is not always better. Clear,

accurate -- keep those words in mind along with emphasizing connections

to background economic ideas (this isn't journalism class, it's

econ). You are encouraged to refer to other sources that may

enhance your understanding and presentation. There will be 2

graduate teams with more difficult material (some weeks).

Exams: These will be two short answer/multiple choice

tests.

Miscellaneous

Students with disabilities who require accommodation (academic

adjustments and/or auxilary aids or services) for this course must first

contact the Office of Student Disability Services in DUC A-200.

Last day to drop the course with a W is listed in the WKU Academic

Calendar.

Note: If a link is dead, please email me as soon as possible. Use Wikipedia, Investopedia, or similar sources to look up terms and concepts

Some articles, if accessed from off-campus, require going through WKU's E-Journal system. Go here http://www.wku.edu/Library/ejrnloff.htm# for instructions

Week 1 (Jan 28) Administration & Basic Ideas in MacroFinance & Market Microstructure I

Class Administration

MacroFinance and Time Series Data Background

Using Stat Software

Assignment for Next Week: Statistical Primer Using Gretl and data sets Shiller Monthly Stock Data (Gretl) Shiller Annual Stock Data (Gretl)

(Use GA Assistance and Gretl Primer)

All

Students:

A1) Open Gretl and become comfortable with key features

(opening files, generating new variables, generating stats, opening command log, using console)

A2) Open

the Shiller Monthly file, and compute real (CPI

adjusted) values of SP, GDP, and PCE by multiplying each variable by the

present CPI (2014=238) and dividing by the CPI in each period

A3)

Generate (annual) percent changes (example: SPrpca =

(SPr-SPr(-12))/SPr(-12) ) for real SP500 Index, real GDP, and real

Personal Consumption

Expenditures (for small differences apx equal to d(logSPr)

A4) For the following sample periods generate summary statistics for

these variables (use the console and summary command to do them all at once)

1871.01-2013.12: SPrpca

1947.01-2013.12: SPrpca, gdprpca, pcerpca

A5) By hand calculate the "Sharpe Ratio" of

each variable = Mean/Standard Deviation

A6) Print (clearly) brief

answers to the following questions on the back of your printed output

-- What are the mean annual percent changes in these variables?

-- How do the standard deviations compare?

-- How do the Sharpe Ratios compare?

Grad Students:

G1) Run an OLS regression using real SP as the dependent variable

and its 1-period lag as the independent variable; Save the residuals

G2) Run a

regression using the residuals as the dependent variable and their 1-period lag as the independent variable

G3) Select 3

subsample time frames (of at least 3 years); Run the real SP and its lag

regression and see if you can find a period where the coefficient in

the regression differs significantly from 1

G4) Generate a

simulated random walk

-- Open Gretl Console under Tools; smpl

1871.1 1871.1 >series simrw=0 > smpl 1871.2

2013.12 >genr simrw =

simrw(-1) + randgen(N, 0, 1) >smpl 1871.1 2013.12 >genr

simrw = simrw + 50 (recenters

to 50)

-- Run the same regression for

this variable, the ADF, and Print a time series plot for it

G5) Prepare 2-3

Powerpoint slides explaining what G1-G3 mean

Related Links: Fama MN Fed Interview Fama AEI Interview (starts in middle) coin flipping

Week 2 (Feb 4 ) Stocks, Random Walks, and Efficient Markets

Reading Quiz: Efficient Capital Markets -- CEE Cochrane on Fame and ME Wiki on Present Value

Related Links: Shiller Data Site Mehra on Equity Premium The Mismeasurement of Risk Barro Disasters NBER Macro Finance Puzzles (p. 2-3 only)

All Students (undergrads utilize GA assistance as needed):

A1) Run a regression with SP500 annual returns in percent (spreturn) and its one period lag

A2) Run a regression with SP500 annual returns and 1-period lag of Shiller PE ratio (peratio) as independent variable

A3) Print (clearly) brief answer to the following questions on the back

of your printed output

-- Do one month lagged returns in stock returns or one month lagged price-earnings

ratios help predict current percent changes in stock returns?

-- What does this appear to indicate about using current information to predict future stock prices?

Grad Students:

G1) Compute 5 year average SP real returns t+1 to t+5 (e.g. spreturn5 =

(spreturn(1) + spreturn(2) + spreturn(3) + spreturn(4)

+spreturn(5))/5 )

G2) Run regressions with 5 year average returns as the dependent variable and

with Shiller's PE ratio (in current year) as the independent variable

G3)

Run regressions with 5 year percent changes in earnings as dependent

variable and with Shiller's PE ratio (in current year) as the

independent variable

G4) Print your results and write a short explanation on the back as to what you found and what it means

Week 3 (Feb 11) Beyond Random Walks, Predictability of Stock Prices

Reading Quiz: Cochrane on Efficient Markets Today

Week 4 (Missed Due to Snow Day)

Revised Week 5 (Feb 25) Topics on Stock Prices

Reading Quiz: Bubble, Bubble (frb-stl) Tulipmania (JSTOR link through WKU)

Vox Barro on Disasters and Equity Premium

Related Links: Bubble Regressions Campbell Bubble in Bond Market? Stock Market Crashes and Depressions (Barro and Ursua) Shiller and Fama NPR Interview

Assignment for Next Week: Fama-Bliss Data Gretl Data

All Students:

A1) Suppose the price of a 1 year bond is 98 and it pays nothing until

the end of the 1 year, show how to calculate its yield (interest) rate (wiki)

A2) Compute summary statistics on 1 year bond return (returntb1), 10 year bond return (returntb10yr), and SP 500 (returnsp) measured as nominal annual percent changes

A3) Generate a time plot of these series

A4) Generate the correlation coefficient between these three variables

A4) Print the output and summarize the relationships

Graduate Students:

G1) Generate a time plot of y1, y2, f2, f2y1 yy21

G2) On back of plot, draw a simple graphic illustrating the meaning of y1, y2, f2

(Note: y1 = actual 1 yr rate; y2=actual 2 year rate; f2 = implied 1 year rate in year)

(Note: f2y1 = difference in f2 and y1; meaning the difference in implied 1 year rate in year 2 and actual 1 year rate)

(Note: yy21=difference in y2 and y1; meaning the difference in actual 2 year rate and actual 1 year rate)

Revised Week 6 (Mar 4) Interest Rates, The Term Structure, and Risk

Reading Quiz: Bond Valuation Understanding the Term Structure of Interest Rates (StL Fed) Wiki on Yield Curve Wiki on Forward Rates

In Class Empirical Studies (not part of assignment)

-- Regress yy21 as dependent variable on f2y1 as

independent

-- Regress yy51 as dependent variable on f5y1 as independent

-- Before Fama-Bliss, the

expected coefficients on the regressions above were 1.0 with high R2

-- After Fama-Bliss ... G4) Prepare a few slides explaining your explorations

-- Regress rx2 as dependent variable on fy21

-- Regress rx5 as dependent variable on fy51

-- Comparing Estimates of Risk Premia e400 Return and Risk Premia Data

Week 7 (Mar 11) Spring Break

Week 8 (Mar 18) Exam I

Week 9 (March 25) Debt Basics & Background

Reading Quiz: 800 Years of Financial Folly (VoxEU) Modigliani-Miller Theorem (Wiki) Cochrane Model of Govt Liabilities

Related Links: Debt Basics PPT Crisis of 2008 PPT

Assignment for Next Week: Cross Country Interest Rates & Debt/GDP Ratios

Data: OECD MacroFinance Data (Excel File with explanation of Country Codes)

Note: The OECD data file is a panel data 1961-2013 for OECD

members (included only in years of membership). It merges (some)

variables from IMF's World Economic Outlook database, World Bank

World Development Indicators database and Global Financial Development

database. This last one (GFDD) is the most useful on this

assignment. In the Gretl file, these variables have names from

data11 to data104 and appear at the bottom of the datafile. All

variables have labels. Gretl doesn't handle text input so Country

Codes are just numbers in the Gretl file. Names appear with Codes

in the Excel file.

All Students

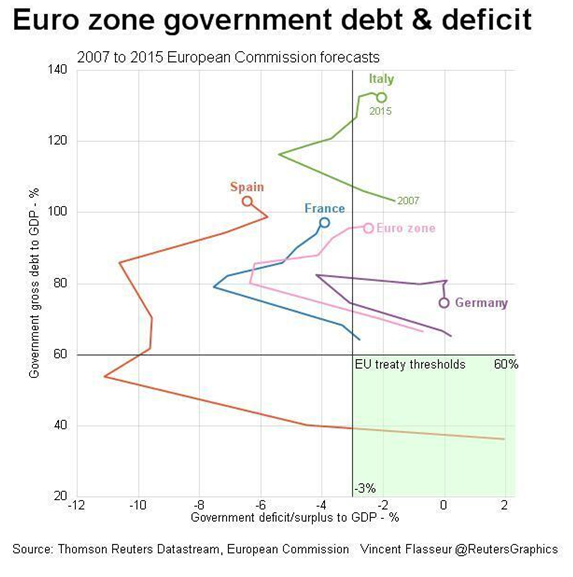

A1) Generate time series plot of the Debt/GDP ratios for the US, Japan, Italy, Spain, France, Germany, Greece (use variable #133 in Gretl file)

Grad Students

G1) Run a regression for country interest rate on long run bonds (variable #212) imitating the one in Hamilton's fiscal tipping points (Debt/GDP, Debt/GDP^2, Current Account/GDP, CA/GDP^2)

Current Account to GDP is variable #121

G2) Run the regression again but put in country specific dummy variables (country fixed effect)

G2) Generate a PPT presentation of your results and address these questions:

-- why use the square of debt/GDP?

-- what role does the country fixed effect play?

-- how do the results change with country effects?

Week 10 (April 1) Sovereign Debt & Fiscal Tipping Points/Risks in U.S.

Reading Quiz: Fiscal Tipping Points US Looming Disaster US

Related Links: S&P Global Credit Risk Report Goff PPT on Crisis

Week 11 (April 8) Assessing Current/Future Global Risks from Debt

Reading Quiz: US EU Japan Bass Chicago CGSB Video

Related Links: S&P Global Credit Risk Report SoberLook 1 SoberLook2 Predicting Sovereign Debt Crisis

Week 12 (April 15) Assessing Risks to U.S. States from Fiscal Imbalance

Reading Quiz: America's Greece (Economist) Joshua Rauh Podcast

Related Links: S&P State Ratings over Time State Ratings Map Rauh & Novy-Marx NBER on States Crisis in Local Pensions (Rauh)

Excel File with Kentucky Data Needed Quantity of Govt Debt (Prescott)

Assignment for Next Week: Interest Rate Data

All Students:

A1) Compute changes differences in the yield curve (10 year Treasury Bond rate minus) 1 year Treasury rate

A2) Generate a time series plot of annualized percent changes in industrial production (indpropca), the term difference variable from step 1, and recessions

A3)

Grad Students

G1) Restrict the sample to periods where the recession variable equals 1 and then with recession variable equals 0

G2) Recompute the the summary statistics and correlations for these the recession and non-recession sub-samples

G3) Compute the correlation matrix for the various risk premia variables (see labels)

G4) Regress recession as the dependent variable against each of the risk premia variables

G3) Print the output and summarize the differences in relationships between these variables in recession and non-recession periods and the regression evidence

Week 13 (Apr 22) Yield Curve Spreads as Key Market Signals

Reading Quiz: Yield Curve (Wiki through relationship to business cycle) Decoding Messages (Richmond Fed)

Related Links: Yield Curve as Predictor of Recessions (NY Fed)

Assignment for Next Week: Rent-Sales Price Ratio, Gold-Silver Prices Housing Data

(The housing data is from Shiller. It lists a

housing price index (HPI) and rental price index (CPIRENT) for

1914-2013)

All Students:

A1) Compute a time plot of housing price index and rental price index (on same plot)

A2) Compute a housing price to rent price ratio using 1980 as the base year (ratio = 100 for 1980)

A3) Compute a gold to silver price ratio using 1980 as the base year again

A4) Generate time plots for the price-rent and for gold-silver price ratios (separate graphs)

-- Print answers to the following questions on the back of the printed output:

-- When are these ratios unusually high and low?

-- How did the gold-price ratio behave before,

during, and after the financial crisis of the fall of 2008?

Grad Students: Gold Silver Data

(The metal prices data is monthly from 1968.1 to

2014.1. It lists prices of gold and silver in dollars per ounce)

G1) Generate a time plot of gold prices and silver prices (on same plot)

G2) Regress the log of silver prices as the dependent

variable with the log of gold prices as the dependent variable; save the

residuals

G3) Plot the residuals

G4) Regress the residuals on their one period lagged

values

G5) Using the plots for all students, the estimates in steps 1-3, as well as adding other variables to the data set,

-- when are gold prices high relative to silver and vice versa?

-- do the residuals tend to return to zero?

-- does changing the time frame make any difference?

-- are the residuals predictable by some other variable?

G6) Generate a 10 min PPT explaining your findings and answers

Week 14 (Apr 29) Spreads and Ratios as Key Market Signals

Reading Quiz: Arbitrage (Wiki to section on "Types") Cointegration (Wiki) Manhattan Prices & Rents (NY Fed)

Week 16 Finals

Does Fed Control Rates (Fama)

FRB Boston Why So Many Bad Real Estate Decisions? Hamilton May 08 Dallas Fed on Real Estate Prices More Dallas Fed (Grad Only)

Related Links: Error Correction Model of M2 Richmond Fed Gold Silver Price Rent Graphics

Topics in Market Microstructure: Market Making, Transactions Costs, Bid-Ask Spread

Reading Quiz: Wiki Market Maker Bid Ask Spread NYSE CBOT Bond Market Foreign Exchange Market FIX

Jenkins: What do Shareholders maximize

Related Links: NYSE CME Group Yahoo Finance

Assignment for Next Week:

Grad Students:

G1) Select one of the 3 items below. Prepare a 10 minute PPT presentation explaining the issue and the economics behind it. You may work in 2 person teams. I have listed links as starting points. You should do some investigative work from there

-- Futures Market Speculation and Spot Price Bubbles Streetwise Professor and Econbrowser (James Hamilton) for posts between 2008 and 2012

-- Centralized Clearing Streetwise Professor for posts over last 6 years (look under counterparty risk also) Hamilton June 08 + Hamilton (Nov 09)

-- Front-Running WSJ Book Review Streetwise Professor

-- Insider Trading Restrictions Insider Trading Debates + CEE on Insider Trading

Assignment for Next Week: Measuring Financialization and Its Impact OECD MacroFinance Data (Excel File with Country Codes)

All Students

1) Generate a time series plot of data103 (stock market capitalization

to GDP) for US, UK, Iceland, and one country of your choosing

Grad Students

G1) Construct two measures of the degree of financialization of an economy (services-based, asset or liability based)

G2) Using plots, summary stats, and/or regressions, show how the

financial crisis of 2008 impacted countries with low, medium, and high

degrees of financialization (by one of your measures)

Related Links: Related Links: S&P Global Credit Risk Report Predicting Sovereign Debt Crisis Goff PPT on Crisis Modigliani-Miller Japan US SoberLook 1 SoberLook2

Financialization and Debt (How Much Is Too Much)

Reading Quiz: Cochrane on Financialization Crisis & Finanicalization in UK, US, Iceland Jenkins on Cyprus

Related Links: Crisis Timeline Goff PPT on Crisis Systemic Risk & Financial Crisis Bubbles or How Unusual Stock Market of 2008 Crisis and Bank Opaqueness

Demographic Shifts and Markets

Key Questions: What impacts will demographic shifts have on asset values?

How accurate are long run demographic predictions?

Data on Demographics and Stock Values: Vox Demographics and Stock Predictability + "Future Shock" + Milken Rebuttal

The Search for Safe Assets

Key Questions: What assets do people seek out when markets are troubled?

What

are attributes of these assets that are common and what are different

(up/down movements; variance; ...)?

Beckworth Post

Search

out references on forces behind gold and silver prices; Present data on

movements of these series (and their ratio and difference); examine the

cointegration of these time series (be careful with unit of time);

Financialization

Key Questions: Did the financial industry grow too large?

What

changes to the financial industry might best reduces changes of future

bubbles/crashes?

See as well as WSJ article on Cyprus that I sent by Holman Jenkins; Explore/examine World Financialization Data

CBO Budget Outlook to 2012 Conference on Looming Fiscal Crisis Unpleasant Monetarist Arithmetic (Cochrane)

Needed Quantity of Government Debt (Prescott) Barro on Ricardian Equivalence

FRB Richmond Econ of Sovereign Defaults

Jenkins WSJ - None Dare Call it Default Monetary Challenges Unpleasant Monetarist Arithmetic (Cochrane)

Why are FX rates hard to predict or explain?

Fx Rates: Why are FX Rates Hard to Predict + FX Rate Conundrum Micro-Macro Disconnect and PPP or Can Oil Prices Forecast Exchange Rates

Related Links: Rational Speculation & Exchange Rates (JME) Conflicts and Commodity Prices Exchange Rates and Business Cycles

MacroFinance Policy Issues & Questions

Key Questons:

Assignments/Presentations: Undergrads read 3 of following articles. Grad students read all plus Robust Capital. Assemble a 10 minute PPT that addresses 1) source(s) of 2008 crash; 2) Fed reactions to crash; 3) Future Policy Changes/Improvements. Don't simply do a summary. Read/assess/weigh the points and try to come to your own conclusions

Boston Fed President on Crisis & Policy William Poole Key Questions about Fed Actions (Book Review) Cochrane on Financial Crisis and Policy + Hamilton Reply

NY Fed President Lessons from the Crisis Jenkins Next Bailout the Last Taming Too Big To Fail (Dallas Fed Speech)

Grad Student Extra: Robust Capital Regulation

Measuring Bank Specific Systemic Risk Influences on Systemic Bank Risk Fed Reactions to Crisis (Dallas Fed)

Does CEO Pay Make Economic Sense? Is CEO Pay Really Inefficient? CEO Pay Jenkins (Reply to Question) CEO Pay Reynolds

How Sustainable/Unstustainable Is Kentucky's Long Run Fiscal Situation? Excel File on KY (update for 2012; for more info see KTRS report Financial or Actuarial http://ktrs.ky.gov/05_publications/index.htm

How Much Did the Size of a Nation's Financial Sector (finanialization) Matter for the 2008 crash and Why: World Financialization Data

Examining the Relationship between Gold & Silver Prices since 2007

Relationships between Stock Prices and Commodity Prices

Similarities and Differences in the Crashes of 1929 and 2008

Ideas and Policies for Regulation of Systemic Risk: Vox Critical Assessment Dodd-Frank Zingales - JAcctResearch May 2009)

Do Central Banks (such as the Fed) Increase or Decrease Systemic Risk?

Insider Trading: Insider Trading Debates + CEE on Insider Trading

Convergence and Divergence in Eurozone Bond Spreads and What's Down the Road?

Was There a Real Estate Bubble and How Would One Decide? Shiller Real Estate Data

What's Been Driving Commodity Pricing: Hamilton June 08 + Hamilton (Nov 09) + SWP Stuck on Stupid + SWP Reply to Hamilton + Vox on Financialization of Commodities

Commodity Price Boom in Perspective Did Easy Money Fuel Commodity Boom

Limits on Short TransactinsOverstock.com; Limits on Short TransactionsInvestopedia

SEC Study on Marked to Market Accounting

Debates about Financial Market Regulation Part 2

Wiki Terms: Clearinghouse; Counterparty Risk; Principal-Agent Problem

Undergrad Assignment (15 min. PPT on Core Issues in Financial Market Regulation & Analysis of Dodd-Frank Legislation

( ; Krozner Corporate Governance CEE (SWP - Agency Problems 9-09)

Grad Assignment: Basics of Clearinghouses

and Reasons for and Against Centralized Clearinghouse System (See

above + Wiki and SWP - Counterparty Risk 8-09 SWP - 5-09)

Related Links: Criminalizing Agency Costs Homan Jenkins (WSJ articles); Overview of Issues in Corprate Governance (frb-ny 2002)

Squam Lake Working Group on Financial Regulation (Clearinghouses; Overall; ...)

(SWP 1-09)

{kind=link}