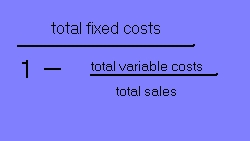

or it may be calculated on

a number of units basis, such as:

( must have unit data to calculate

breakeven point in terms of units)

sales price per unit x number

of units = total fixed costs + variable cost per unit x number of units

or:

SP * X = FC + VC * X

(SP-VC) * X =FC

X= FC/(SP-VC)

where SP = sales price per

unit

FC= total fixed costs

VC=variable cost per unit

X= units to breakeven

the term, (SP-VC) = contribution margin per unit

therefore, breakeven point in terms of units equals fixed costs divided by contribution margin per unit.

To determine what sales level it takes to generate a certain level of income, treat the income desired as an additional fixed cost in the numerator.

If a certain income is desired after tax, first convert the after-tax income to a before tax income equivalent by dividing the after-tax income by ( 1-tax rate)