The

world economy is in trouble, and governments are making things

worse.

Here's the story, right out of the pages of the 2012 Index of Economic Freedom,

published Thursday by the Heritage Foundation and The Wall Street

Journal:

"Rapid

expansion of government, more than any market factor, appears to be responsible

for flagging economic dynamism. Government spending has not only failed to

arrest the economic crisis, but alsoin many countriesseems to be prolonging

it. The big-government approach has led to bloated public debt, turning an

economic slowdown into a fiscal crisis with economic stagnation fueling

long-term unemployment."

The

new index documents a world in which economic freedom is contracting, hammered

by excessive government regulations and stimulus spending that seems only to

line the pockets of the politically well-connected.

Government spending rose on average to 35.2% of gross domestic product (GDP)

from 33.5% last year as measured by the 2012 index.

Enlarge

Image

Most

of the decline in economic freedom was in countries in North America and Europe.

Canada, the United States and Mexico all lost ground in the index, and 31 of the

43 countries in Europe suffered contractions. They

ought to know better. These are the very countries that have led the world-wide

revolution in political and economic freedom since the end of World War II. But

now, weighed down by huge welfare programs and social spending that is out of

control, many governments are expanding their reach in ways more reminiscent of

the 1930s than the 1980s.

How

about the U.S., historically the country more responsible than any other for

leading the march of freedom? Under President Barack Obama, it has moved to the

back of the band. Its economic freedom score has dropped to 76.3 in 2012 from

81.2 in 2007 (on a scale of 0-100). Government expenditures have grown to a

level equivalent to over 40% of GDP, and total public debt exceeds the size of

the economy.

The

expansion of government has brought with it another critical challenge to economic

freedom: corruption. The U.S. score on the index's Freedom

from Corruption indicator has dropped to 71.0 in 2012 from 76.0 in

2007. That's not surprising, given the administration's

excessive regulatory zeal. Each new edict means a new government bureaucracy

that individuals and businesses must navigate. Each new law opens the door for

political graft and cronyism.

There

are some bright spots. Economic freedom has continued to increase in Asia and

Africa.

In fact, four

Asia-Pacific economiesHong Kong, Singapore, Australia and New Zealandtop the

Index of Economic Freedom this year. Taiwan showed

impressive gains, moving into the index's top 20. Eleven of the 46 economies in

sub-Saharan Africa gained at least a full point on the index's economic freedom

scale, and

Mauritius

jumped

into the top 10 with the highest ranking8th placeever achieved by an African

country.

The

2012 index results confirm again the vital linkage between advancing

economic freedom and eradicating poverty. Countries that rank "mostly unfree" or

"repressed" in the index have levels of poverty intensity, as measured by the

United

Nations' new Multidimensional Poverty Index, that

are three times higher than those of countries with more economic

freedom.

Enlarge

Image

AFP/Getty

Images

Taiwan

showed impressive gains, moving into the Index's Top 20.

Countries

with higher levels of economic freedom have much higher levels of per capita GDP

on average. In Asia, for example, the five freest economies have per capita

incomes 12 times higher than in the five least free economies. Economic growth

rates are higher, too, in countries where economic freedom is advancing.

The average growth rate

for the most-improved countries in the index over the last decade was 3.7%, more

than a point-and-a-half higher than in countries where economic freedom showed

little or no gain.

Positive

measures of human development in areas such as health and education are highly

correlated with high levels of economic freedom, and economically free countries

do a much better job of protecting the environment than their more regulated

competitors. When you actually look at the performance data, it turns out that

the "progressive" outcomes so highly touted by those favoring big government

programs to address every societal ill are actually achieved more efficiently

and dependably by the marketplace and the invisible hand of free

economies.

Unfortunately,

most of the world's

people still live in countries where economic freedom is heavily constrained by

government control and bureaucracy. India and China, with about one-third of the

world's population, have economic freedom scores barely above 50 (a perfect

score would be 100). In a globalized world, both countries are

benefiting from the trade and investment liberalization that has taken place

elsewhere. But sustained long-term growth will depend on advances in economic

freedom within each of these giants so that broad-based market systems may

develop.

The

Index of Economic Freedom has recorded a step back over the last year for the

world as a whole. It was only a small step, with average scores declining less

than a point, but the consequences have been severe: slower growth, fiscal and

debt crises, and high unemployment. The biggest losers have been the economies

in North America and Europe, regions that have led the world in economic freedom

over the years.

The

2012 results show the torch of leadership in advancing freedom passing to other

regions. Whether this is a long-term trend remains to be seen, but it is clear

that if America and Europe do not soon regain trust in the principles of

economic freedom on which their historical successes have been built, their

people, and perhaps those of the world as a whole, are in for dark days

ahead.

Mr.

Feulner is president of the Heritage Foundation and co-editor of the 2012 Index

of Economic Freedom.

The

annual Heritage Foundation-Wall Street Journal Index of Economic Freedom is

released today. Is economic freedom on the cusp of a

renaissance in Asia?

At

first blush, no.

China, now

the largest economy in the region, is firmly on a backward economic-freedom

trajectory. Foreign companies report an increasingly hostile regulatory

environment, and reform in general seems stalled.

Japan, the

next-largest economy, remains mired in political deadlock, and

key liberalization measures such as postal privatization are dead.

India

is

as sclerotic as ever, Indonesia is in danger of retreating on banking reforms it

made post-1997 crisis. Even Hong Kong, again ranked at the top of the

index, is every day in greater danger of abandoning the economic freedoms that

made it prosperous, whether through a proposed competition law or through the

government's sheer inability to resist meddling in this industry or

that.

In

recent months India has

seen fierce debates over corruption and allowing inward investment by foreign

big-box retailers. These issues aroused widespread discussion,

although they haven't yet produced positive policy outcomes. In New Delhi's

defense, the government has quietly opened additional channels for foreign

capital to invest in Indian businesses via stock and bond markets, and this week

it eased rules for foreign single-brand retailers.

Enlarge

Image

Associated

Press

South

Korean President Lee Myung-bak signing bills to implement the country's free

trade deal with the U.S. in November.

South

Korea has

started a pro-freedom rethink of economic policy. Most

visible is Seoul's new enthusiasm for free trade, as seen in the major deals

with the U.S. and European Union that are set to open Korea to a previously

unheard-of degree.

President Lee Myung-bak also has attempted controversial pro-freedom

reforms of labor laws and a liberalization of the media

industry. While these efforts have been only partly successful,

both sparked renewed public debate.

Taiwan

holds

a presidential election Saturday that turns in part on trade and investment

openness to China;

the incumbent candidate, Ma Ying-jeou, touts improved cross-Strait economic

freedom as a key accomplishment of his administration. Indonesia is determinedly if sometimes

inconsistently pushing forward with the fight against business-stifling

corruption.

Then

there's Japan. It fares

poorly in this year's index, with a decline in both its score

and its ranking (to 22 from 20 last year), not least because the government's

fiscal position deteriorated further. But even here there are some tentative

green shoots.

Tokyo

lawmakers recently rebelled against Prime Minister Yoshihiko Noda's plan to

increase the consumption tax. Mr. Noda has elsewhere distinguished himself

through his willingness to push Japan into negotiations for a Trans-Pacific

Partnership trade deal that would mark the greatest opening of the economy since

the late 1940s. And amid the chaos of a post-tsunami nuclear crisis, some brave

souls suggested a major reform of electric utilities. Dare to

dream.

As the

mixed index scores show, these rustlings of economic freedom

in Asia have not always translated into quantifiable policy

outcomes. They must eventually do so to have any impact on

business. Still, each law starts out as

an idea. At

least the right ideas are starting to percolate in many corners of the

region.

More

interesting is the possible explanation. The basic concept of economic freedom

has been in bad odor in many parts of Asia for long spans. Singapore and Japan, despite their

relatively high scores on the index, have always been characterized by a high

degree of government intervention in the business worldand their seeming

success served as an inspiration for others. The echoes

still reverberate. Despite his reformist leanings, Mr. Lee in Korea fell back on

green-tech industrial policy as an element of his post-global-crisis stimulus

plan, to cite only one of many examples.

Yet

there is mounting

evidence that the old, state-led model isn't working out so well. Japan's two

decades of stagnation are the obvious example, and they may

now be causing sufficient desperation to pave the way for freer trade. Korea

fears a similar fate could befall it as the economy reaches First-World levels

and growth rates slow. Some Indians worry that phenomenal growth will slow

before it has really begun unless New Delhi starts another round of

reforms.

This

is good news for business, or anyway it will be if these freedom ideas start

taking root. Asia's

phenomenal growth tends to obscure the destructive tendency of Asian governments

to undermine their entrepreneurial citizens with stifling regulations, often in

the name of encouraging a handful of favored industries, such as export

manufacturing, at the expense of many others.

Greater

economic freedom means unshackling those entrepreneurs, who are necessary for

sustained growth in the future. Asia can't afford not to do

this.

Mr.

Sternberg is an editorial page writer at The Wall Street Journal

Asia.

Wed

Jan 11, 2012 6:32pm GMT

http://af.reuters.com/article/commoditiesNews/idAFL6E8CB55620120111?sp=true

LONDON Jan 11 (Reuters) - The Philippines and Peru will be

among emerging economies that become much more prominent in the next few

decades, helped by demographics and rising education standards, with the

Philippines set to leapfrog 27 places to become the 16th largest economy by

2050, HSBC predicts.

The bank expects China to

overtake the United States as the world's biggest economy by 2050, and says

strong growth rates in other developing countries will help drive the global

economy.

"Plenty of places in the

world look set to deliver very strong rates of growth. But they are not in the

developed world, which faces both structural and cyclical headwinds. They are in

the emerging world," the bank said in its report 'The World in

2050'.

It based its forecasts on

fundamentals such as current income per capita, rule of law, democracy,

education levels and demographic change.

HSBC projects the

Philippines economy is poised to grow by an average of 7 percent annually over

the next 40 years, while Peru should average annual growth of 5.5 percent over

the same period.

The sheer pace of

population growth in countries such as Nigeria and Pakistan means that these

economies will swell in size to be included among the 100 biggest economies even

if their incomes on a per-capita basis remain low.

HSBC said lower

scores for rule of law in Latin America constrained its per-capita inccome

projections for the region though it noted that Brazil was making headway in

this aspect.

"The losers are

the small population, ageing economies of Europe,"

added the bank, which says the demographics in much of Europe underscores

concerns about the debt problems faced by many of the continent's

governments.

'COPY AND PASTE'

If sufficiently open to modern technology, developing

countries could enjoy many years of robust GDP growth although they could

struggle for growth drivers once they have adapted to technological advances,

HSBC said.

"The initial years of

development could be described as 'copy and paste'

growth, as countries open

themselves up and adapt to the world's existing technologies. Once the 'copy and

paste' growth is complete ... many economies struggle and get stuck in what is

often known as the middle-income trap."

"But many of the

countries we are considering are still at such an extremely low level of

development that there are years of this 'copy and paste' growth ahead," it

added.

It was here that many of

the pessimism about China was misplaced, the bank

argued.

"One of the most commonly

cited reasons for concern about China is the high rate of investment as a

percentage of GDP ...(But) we believe the strong rate of investment is entirely

justified - providing China with much needed basic infrastructure," it

said.

The bank said high levels

of education in central and eastern Europe meant that the region could enjoy

strong income per capita growth in the coming years before weak demographics

eventually sap economic growth.

"While education rates

are similar (to the West), the average income per capita in the central and

eastern Europe block is just one fifth that of the developed world. For this

reason ... economies have great scope to catch up in income per capita," it

said.

"Some of the

smaller Eastern European countries - Romania, the Czech Republic and Serbia -

(should) all do extremely well, particularly in the coming decade, before

demographics prove to be more of a drag." (Reporting

by Sebastian Tong; Editing by Susan Fenton)

© Thomson Reuters 2012 All rights

reserved

The

aftershocks, it is clear, will be disrupting global growth for some time. Less

clear is how the turmoil will alter economic strategies in China, India, Brazil

and other fast-growing emerging markets.

Will

they shrug it off? Will it prompt them to turn away from markets in favor of

more muscular government control? Will they evolve a new strain of

capitalismthe Beijing Consensus, perhapsthat becomes a beacon for

others? Is there any well-defined alternative?

In

emerging markets, skepticism and schadenfreude abound. "The old paradigm in

which the smart guys from Europe and America harangue us, wag a finger and tell

us: 'This is what you've got wrong'that's over," says Rajiv Kumar, an Oxford

University-trained economist who is secretary-general of the Federation of

Indian Chambers of Commerce and Industry.

The

global financial crisis exposed shortcomings of U.S.-style capitalism, the

inadequacies of what the British dubbed "light touch" financial regulation and

the system's tendency toward periodic excess. More recently, Europe's

sovereign-debt crisis highlighted the tension of a costly welfare state in the

absence of vigorous economic growth to finance it.

Enlarge

Image

Associated

Press

India's

economic growth skidded to 6.9 % in the July-September quarter, its lowest in

over two years, and is forecast to slow further amid delayed economic reforms

and a worsening global outlook.

Above, an Indian man works at a textile factory in Ahmedabad,

India.

The

U.S. model continues to struggle three years after regulators allowed Lehman

Brothers to fail.

Billions of idle cash sits in U.S. corporate coffers even as millions of workers

remain unemployed for more than a year. The housing market remains in the

doldrums. Political paralysis on fiscal policy undermines the U.S.'s economic

authority. All this and more have weakened the single best argument for the U.S.

economic model: It works.

A few

years back, when Henry Paulson was still U.S. Treasury secretary, Wang Qishan,

China's vice premier, needled him. "Hank, I used to listen to you. You were my

teacher," recalls Mr. Paulson, who visited China often when he was head of

Goldman Sachs Group. "Maybe now my teacher doesn't seem so wise given the

mistakes you made."

Today,

Mr. Paulson adds: "We've given China a flawed model."

The

European model doesn't offer much, either. In one

of the most telling moments of 2011, Klaus Regling, who heads the euro zone's

bailout kitty, was dispatched in search of moneynot to Washington but to

Beijing. The mission didn't produce results. It did, however, provoke bursts of

condescension from some in China about the flaws in the European model.

Jin

Liqun, chairman of the supervisory board of China's sovereign-wealth fund, China

Investment Corp., derided Europe as a "worn-out welfare society" in an

interview with al-Jazeera TV in November.

For

the old-money economies, 2011 was downright humiliating. Here are three points

to ponder:

Who

could have imagined during the worst of the 1990s Asian financial crisis that in

November 2011 the

president of the Federal Reserve Bank of New York, William

Dudley, would tell cadets at the U.S. Military Academy at

West Point: "We can learn from the example of emerging nations that took the

tough decisions necessary to emerge from past crises stronger, more competitive

and better positioned

."

Or that the sovereign

debt of the U.S., Italy, Spain, Portugal, Ireland and Japan would be downgraded

while debt of Angola, Brazil, Bulgaria, Colombia, the Czech Republic, Estonia

and Peru would be upgraded.

Or that the winning

bidder for the Portuguese government's stake in a big electric utility would be

China's Three Gorges Corp., which beat two Brazilian firms and just onea German

companyfrom the entire developed world.

"The

labor laws induce sloth, indolence, rather than hardworking," he said.

"The

incentive system is totally out of whack. Why should

some [euro-zone] member's

people have to work to 65, even longer, whereas in some other countries they are

happily retiring at 55, languishing on the beach? This is unfair."

"The

welfare system is good for any society to

help those who happen to be

disadvantaged to enjoy a good life," he said. "But a welfare society should not

induce people not to work." So much for Europe's "social market."

Japan's

export-driven model, once the envy of nearly every other economy, has been

largely written off, the consequence of a decadelong battle to revive growth.

Coupled with the blow of the Fukushima Daiichi nuclear calamity, wrought by last

March's tsunami and earthquake, and Japan's reputation for competence and

efficiencies was shot.

But is

there a well-articulated alternative to rich-country market capitalism?

Not

yet, says Joseph Nye, a Harvard University political scientist

who has

chronicled the evolution of global centers of power. "It's not like the Cold War

when there was an alternative ideologycommunismor the '30s, when you had two

contenders, communism and fascism."

After

all, most emerging markets today are embracing global capitalism and its

institutions. Russia is

about to join the World Trade Organization, the club of free

traders. China is seeking a bigger, not smaller, role in the International

Monetary Fund, the closest thing the market economies have to a global central

bank.

Niall

Ferguson, the

New York University historian, argues that emerging markets are succeeding by

downloading the "killer apps" of Western civilization. Kenneth Rogoff, the Harvard

University economist, says, "For now, at least, the only serious alternatives to

today's dominant Anglo-American paradigm are other forms of

capitalism." And Robert Zoellick, president of the

World Bank, says China's receptivity to markets means that it's easier to build

a private toll road in Chongqing than in Pennsylvania.

"Everyone

who criticized the system during the bubble years has been vindicated. And the

truth is a lot of bad things happened," says Arminio Fraga, a U.S.-trained

economist, formerly Brazil's central banker and now head of a private-equity

firm. "But a lot of peoples' claims are false. There's a danger that the pendulum

may swing too far in the wrong direction," he said, referring to emerging-market

flirtations with a return to more government management of the

economy.

Still,

if emerging markets are to peel away from the U.S.-Europe-Japan road, this would

appear to be a key moment. Those pondering economic routes that emerging markets

might take divide roughly into three camps.

One

camp sees emerging markets going in a new direction, perhaps inspired by China's

remarkable growth spurt and its mix of government control and market forces.

In a

book newly translated from Chinese, "Demystifying the Chinese Economy,"

Justin Yifu Lin, now chief economist of the World Bank, recalls "widespread

skepticism in international academic circles" when China launched its late-1970s

reforms of offering protection to big state-owned enterprises in "old priority

sectors" while introducing private enterprises into "new labor-intensive

sectors." In his view of history, other developing countries heeded the

"Washington Consensus" to dismantle every possible restraint on

marketsand "ended up in economic collapse and long-term stagnation."

Mr.

Lin, while acknowledging fault lines in Chinese growth, argues that, in general,

"opportunities and challenges facing developed countries differ from those of

developing countries." China, India and other economies with huge labor supplies

should pursue economic strategies different from those pursued by others, an

argument for China's heavy emphasis on promoting investment over consumer

spending and relying on exports to provide jobs.

But as

cracks in the Chinese success story emergescattered uprisings, tales of

spectacular corruption, high-speed rail crashessome of its luster has been

lost. And Francois

Godement, a French specialist in Asia, describes China as split between

competing versions of its own model: the more Western-style move up the

technological value chain, which he calls the Guangdong model after the

prosperous coastal region, and the Chongqing experiment in the center of

China, which is marked by heavy state subsidies and paeans to Chairman Mao.

A

second camp argues

that emerging markets will prosper not by rejecting Western capitalism, but

executing it better,

perhaps finding a way to restrain its tendency toward financial excess while

retaining the efficiency of markets.

"Latin America has tried many models,"

says Liliana Rojas-Suarez, a Peru-born economist now at the Center for Global

Development, a Washington think tank. "This model"markets, private

enterprise, orthodox macroeconomic policies"is working for them."

Ms.

Rojas-Suarez points to Peru's new center-left president, Ollanta Humala, as

support for the second model. She notes that, despite some of his campaign

rhetoric, Mr. Humala hasn't deviated much from the previous government's course.

After all, Peru's economy grew a robust 8.8% in 2010 and 2011 growth is

forecast at 6.7%. "The

cost for a leftist government to change what is seen, so far, as a success is

just too large," she says.

Ernesto

Zedillo, the former president of Mexico, now teaching at Yale

University,

contends that Europe has failed to see what Mexicans understand about responding

to a financial crisis. "Latin America, after so many years, has learned its

lessons," he says. "In

the '80s, when we behaved just like the Europeans today, we were always behind

the curve." In the 1990s, he says, that wasn't so.

The

conclusion he drew, and repeated ever since: Markets overreact, so government

policy must overreact even more. Rich countries haven't heeded that lesson, he

says, bemoaning "the slowness, the parsimony, the hesitation, the political

conflict we have seen in Europe and in the U.S."

A

third camp sees what

the World Bank's Mr. Zoellick calls "ruthless pragmatism," an almost

ideology-free quest for results that will borrow freely from around the

world.

In

this vein, Olivier Blanchard, a France-born Massachusetts Institute of

Technology professor and now chief economist at the IMF, says: "If I were a

young, emerging-market country, my motto would be: Go slow."

He

advises them to develop a modern financial system slowly, adopting innovations

only as they are proven elsewhere and lowering barriers to foreign capital only

gradually. And he would

craft rules for labor markets with care to avoid the sclerosis plaguing some

richer economies. "Institutions have a life of their own," he

says.

From

his travels around the globe, Mr. Zoellick concludes: "People are looking for what works. It

was very important that you had a model that started to work in Japan, Korea,

Taiwan and then spread to others in Southeast Asia and China."

Have

emerging markets concluded that the U.S. and European models don't work? "Not

yet, but they could," he says. It depends whether the U.S., Europe and Japan

sort out their problems in the next several years.

Write

to David

Wessel at capital@wsj.com

Presenting

an annual investment outlook is a hazardous task. At the start of 2011, investors were

warned to eschew the bond market. Pundits described the low yields of U.S.

Treasuries as a "bond market bubble." In fact, if you had bought 30-year U.S.

Treasury bonds at the start of the year when they yielded 4.42% and held them

through 2011, when the yield had fallen to 2.89%, you would have earned a 34%

return.

Meanwhile,

U.S. stocks stayed flat, Europe and Japan declined by double digits, and

emerging markets suffered even greater losses. Last year again demonstrated that

it is virtually impossible to make accurate short-term predictions of asset

returns.

But it

is possible to make reasonable long-term forecasts. Let's start with the bond market. If

an investor buys a 10-year U.S. Treasury bond and holds it to maturity, he will

make exactly 2%, the current yield to maturity. Even if the inflation rate is

only 2%, the informal target of the Federal Reserve, investors will have earned

a zero rate of return after inflation.

With a

higher inflation rate, U.S. Treasurys will be a sure loser.

Other high-quality U.S. bonds will fare little better. The yield on a total U.S.

bond market exchange-traded fund (ticker BND) is only 3%. Bonds, where long-run

returns are easy to forecast, are unattractive in the U.S. and Japan, as well as

in Europe, where defaults and debt restructurings are

likely.

Long-run

equity return forecasts are more difficult, but they can be estimated under

certain assumptions. If

valuation metrics (such as price-earnings ratios) are constant, long-run equity

returns can be estimated by adding the anticipated 2012 dividend yield for the

stock market to the long-run growth rate of earnings and dividends. The dividend

yield of the U.S. market is about 2%. Over the long run, earnings and dividends

have grown at 5% per year.

Thus,

with no change in valuation, U.S. stocks should produce returns of about 7%,

five points higher than the yield on safe bonds.

Moreover, price-earnings multiples in the low double digits, based on my

estimate of the earning power of U.S. corporations, are unusually attractive

today.

Stocks

were losers to bonds in 2011. But don't invest with a rear-view mirror.

U.S. stocks, available

in a broad-based index fund or ETF, are more attractive than bonds today. The

same is true for multinational corporations throughout the

world.

Investors

in retirement, who desire a steady stream of income, can purchase a portfolio

through mutual funds or ETFs tilted toward stocks paying growing dividends, with

yields of 3% to 4%. And some areas of the bond market are attractive for

investors who want some fixed-income investments. Tax-exempt funds that trade on

exchanges (so called closed-end investment companies) that take on moderate

amounts of short-term debt to increase the size of their portfolios have yields

of 6% to 7%, and emerging-market bond funds have generous

yields.

Enlarge

Image

Corbis

Emerging

markets offer the best prospects for both equity and bond returns over the next

10 years. A

number of fundamental factors favor the emerging economies. While Europe and the

U.S. struggle with debt-to-GDP ratios of 100% or moreand Japan's ratio is

250%the fiscal

balances of the emerging economies are generally favorable, and debt ratios are

low. Low debt levels encourage economic

growth.

Demography

also favors the emerging economies.

Dependency ratios

(nonworking age to working age population) are far more favorable in emerging

markets. Soon Japan will have as many

nonworkers as workers, and Europe and the U.S. are not far behind. Emerging

markets, such as India and Brazil, will continue to have two to three workers

for every nonworker. Even China, with its one-child policy, will

have favorable demographics and a large potential labor force until at least

2025. Countries with

younger populations tend to grow faster.

Natural-resource-rich

countries will also benefit over the decade ahead. The

world has a finite amount of natural resources and the relative prices of

increasingly scarce resources will rise. Countries such as Brazil, with

abundant oil and minerals, as well as water and arable land, will benefit from

the world's increasing demand.

Emerging

stock markets were among the worst performers in 2011 despite their favorable

economic performance and future outlook. Hence their stock valuations are

unusually attractive relative to developed markets.

Historically, emerging-market equities had price-earnings multiples 20% above

the multiples for the S&P 500. Today, those multiples are 20% lower. And

emerging-market bonds have significantly higher yields than those in developed

markets.

Much

worry has been expressed about real-estate prices and construction activity in

China. "It's Dubai times 1,000," says one hedge-fund manager who predicts an

economic collapse. Obviously, an end to China's growth would be a significant

blow to the world economy.

But

parallels to the U.S. real-estate bust and the resulting damage to the economies

and financial institutions of the Western world seem unwarranted. The absorption of vacant space

remains extremely high in China, where hundreds of millions more people are

expected to move from farms to cities. And unlike the U.S., where people bought

new homes with little or nothing down, Chinese buyers make minimum down

payments of 40% on a new home (and 60% on a second home).

In the

U.S., savings rates fell to zero, and consumer-debt levels tripled relative to

income. In China,

savings rates as a percentage of income are one-third.

Most

important, the government has the wherewithal and the flexibility to stimulate

the economy and recapitalize banks if necessary. China has a debt-to-GDP ratio of

only 17%. China's growth will slow down from the breakneck

pace of the last several years. But it will continue to grow rapidly, and a

meltdown of the Chinese economy is highly unlikely.

The

U.S. housing bust has made the single-family home an extremely attractive

investment. House prices have fallen sharply, and 30-year mortgages are available for

people with good credit at rates below 4%. Housing affordability has never been

better.

Whatever

the specific mix of assets in your portfolio at the start of 2012, you would do

well to follow one crucial piece of advice. Control the thing you can

controlminimize investment costs. That is especially important in a low-return

environment. Make low-cost index mutual funds or ETFs the core of your portfolio

and ensure that any actively-managed investment funds you purchase are

low-expense as well.

Mr.

Malkiel is the author of "A Random Walk Down Wall Street" (10th ed., paper, W.W.

Norton, 2012).

Planet

Money reports

on a new OECD study that finds that income inequality is rising worldwide within

most countries:

Planet

Money cites three possible explanations given in the OECD study for the

trend:

1.

Robots, etc.

Trade

barriers have come down. Technology has advanced. The combination of these two

factors has disproportionately benefited highly-skilled workers. You want to be

the guy building the robot, not the guy whose job got replaced by a

robot.

2.

Rich people marry rich people

Inequality

is calculated by household, not by individual. And a few changes at the

household level have driven some of the increase in

inequality.

For

one thing, its become more common for people to choose spouses in their own

income bracket. In other words, rich people are now more likely to marry other

rich people, and poor people are more likely to marry other poor people.

(Theres a creepy term for this: assortative mating.)

Single-parent

households and single-person households without children have also become more

common. Both groups are disproportionately likely to be at the bottom of the

income ladder.

3.

Free-wheeling job markets

State

ownership of corporations has declined. Price controls have become less common.

Minimum wages have fallen relative to average wages. Legal changes have made it

easier to fire temporary wokers.

Taken

together, these changes have actually improved overall employment levels.

(Businesses are more likely to higher hire workers when they can pay lower wages

and when its easier to fire people.)

But

despite the gain in employment, the same shifts may also have driven up

inequality. In the words of the report, the high-skilled reaped more

benefits from a more dynamic economy.

That

last explanation is the Paul Krugman explanation. In the 1950's we had less

competition and less economic freedom. Unions were more powerful protecting

workers. Were living in a libertarians paradise and of course, the rich get

richer and the poor get poorer. I

reject that interpretation of what unions actually

do,

but even if you agree with Krugman, is it really the case that Sweden and other

countries have reduced their legal protections for

workers?

There

is a fourth explanation. The fourth explanation is that these results are

statistical anomalies. They

come from how

we calculate inequality using household income. The underlying cause of the

worldwide trend is an increase in the divorce rate that caused an abrupt change

in the number of households and an unexpected increase in the labor force

participation of married women. It is not a result of a dysfunctional economy or

a dysfunctional political system or technological change. Its the result of an

increase in the availability of the pill and other forms of birth control that

changed the sexual and marital culture leading to a world where divorce is much

more common.

UPDATE:

Oops. My fourth explanation is partially embedded in the second explanation

given above. I read the heading Rich marrying the rich and missed the part

about single-parent and single-person households. HT to Jacob Goldstein for

pointing that out.

http://www.project-syndicate.org/commentary/rogoff88/English

|

34 |

2012-01-02

Rethinking the Growth

Imperative

CAMBRIDGE

Modern macroeconomics often seems to treat rapid and stable economic growth as

the be-all and end-all of policy. That message is echoed in political debates,

central-bank boardrooms, and front-page headlines. But does it really make sense

to take growth as the main social objective in perpetuity, as economics

textbooks implicitly assume?

Certainly,

many critiques of standard economic statistics have argued for broader measures

of national welfare, such as life expectancy at birth, literacy, etc. Such

appraisals include the United Nations Human Development Report, and, more

recently, the French-sponsored Commission on the Measurement of Economic

Performance and Social Progress, led by the economists Joseph Stiglitz, Amartya

Sen, and Jean-Paul Fitoussi.

But

there might be a problem even deeper than statistical narrowness: the failure of

modern growth theory to emphasize adequately that people are fundamentally

social creatures. They evaluate their welfare based on what they see around

them, not just on some absolute standard.

The

economist Richard Easterlin famously observed that surveys of happiness show

surprisingly little evolution in the decades after World War II, despite

significant trend income growth.

Needless to say, Easterlins result seems less plausible for very poor

countries, where rapidly rising incomes often allow societies to enjoy large

life improvements, which presumably strongly correlate with any reasonable

measure of overall well-being.

In

advanced economies, however, benchmarking behavior is almost surely an important

factor in how people assess their own well-being. If so, generalized income growth might well

raise such assessments at a much slower pace than one might expect from looking

at how a rise in an individuals income relative to others affects her

welfare. And, on a related note, benchmarking behavior may well

imply a different calculus of the tradeoffs between growth and other economic

challenges, such as environmental degradation, than conventional growth models

suggest.

To

be fair, a small but significant literature recognizes that individuals draw

heavily on historical or social benchmarks in their economic choices and

thinking. Unfortunately, these models tend to be difficult to manipulate,

estimate, or interpret. As a result, they tend to be employed mainly in very

specialized contexts, such as efforts to explain the so-called equity premium puzzle (the

empirical observation that over long periods, equities yield a higher return

than bonds).

There

is a certain absurdity to the obsession with maximizing long-term average income

growth in perpetuity, to the neglect of other risks and considerations. Consider

a simple thought experiment. Imagine that per capita

national income (or some broader measure of welfare) is set to rise by 1% per

year over the next couple of centuries. This is roughly the trend per

capita growth rate in the advanced world in recent years. With annual income

growth of 1%, a generation born 70 years from now will enjoy roughly double

todays average income. Over two centuries, income will grow

eight-fold.

Now

suppose that we lived in a much faster-growing economy, with per capita

income rising at 2% annually. In that case, per capita income would

double after only 35 years, and an eight-fold increase would take only a

century.

Finally,

ask yourself how much you really care if it takes 100, 200, or even 1,000 years

for welfare to increase eight-fold. Wouldnt it make more sense to worry about

the long-term sustainability and durability of global growth? Wouldnt it make

more sense to worry whether conflict or global warming might produce a

catastrophe that derails society for centuries or more?

Even

if one thinks narrowly about ones own descendants, presumably one hopes that

they will be thriving in, and making a positive contribution to, their future

society. Assuming that they are significantly better off than ones own

generation, how important is their absolute level of

income?

Perhaps

a deeper rationale underlying the growth imperative in many countries stems from

concerns about national prestige and national security. In his influential 1989 book The

Rise and Fall of the Great Powers, the historian Paul Kennedy concluded

that, over the long run, a countrys wealth and productive power, relative to

that of its contemporaries, is the essential determinant of its global

status.

Kennedy

focused particularly on military power, but, in todays world, successful

economies enjoy status along many dimensions, and policymakers everywhere are

legitimately concerned about national economic ranking. An economic race for

global power is certainly an understandable rationale for focusing on long-term

growth, but if such competition is really a central justification for this

focus, then we need to re-examine standard macroeconomic models, which ignore

this issue entirely.

Of

course, in the real world, countries rightly consider long-term growth to be

integral to their national security and global status. Highly indebted

countries, a group that nowadays includes most of the advanced economies, need

growth to help them to dig themselves out. But, as a long-term proposition, the

case for focusing on trend growth is not as encompassing as many policymakers

and economic theorists would have one believe.

In

a period of great economic uncertainty, it may seem inappropriate to question

the growth imperative. But, then again, perhaps a crisis is exactly the occasion

to rethink the longer-term goals of global economic

policy.

Kenneth

Rogoff is Professor of Economics and Public Policy at Harvard University, and

was formerly chief economist at the IMF.

Copyright:

Project Syndicate, 2012.

www.project-syndicate.org

You

might also like to read more from Kenneth

Rogoff or return to our

home

January

4, 2012

Away

from the low growth and high regulation of an America under Washington's thumb,

our northern neighbor is economically strong. As 2011 ends, Canada has

announced yet another tax cut -- and will soar even more, says Investor's

Business Daily.

It's

not just that Canada's conservative government favors makers over takers.

Canada's

incomes are rising, its unemployment is two percentage points

below the U.S. rate, its currency is strengthening and it boasts

Triple-A or equivalent sovereign ratings across the board from the five top

international ratings agencies, lowering its cost of

credit.

Is it

too much to ask Washington to start paying attention to the Canadian success

story?

Source:

"Tax Cuts, Less-Intrusive Gov't Help Canada Soar," Investor's Business Daily,

December 29, 2011.

For

text:

http://news.investors.com/Article/596263/201112291827/tax-cuts-give-canada-economy-a-boost.htm

It

used to be so cool to be wealthyan elite education, exclusive mobile

communications, a private screening room, a table at Annabel's on London's

Berkeley Square.

Now it's hard to

swing a cat without hitting yet another diatribe against income inequality.

People sleep in tents to protest that others are too damn wealthy.

Yes,

some people have more than others. Yet as far as millionaires and billionaires

are concerned, they're experiencing a horrifying revolution: consumption

equality. For the most part, the wealthy bust their tail, work

60-80 hour weeks building some game-changing product for the mass market, but at

the end of the day they can't enjoy much that the middle class doesn't also

enjoy. Where's the fairness? What does Google founder Larry Page

have that you don't have?

Luxury

suite at the Super Bowl? Why bother? You can recline at home in your massaging

lounger and flip on the ultra-thin, high-def, 55-inch LCD TV you got for

$700and not only have a better view from two dozen cameras plus Skycam and fun

commercials, but you can hit the pause button to take a nature break. Or you can

stream the game to your four-ounce Android phone while mixing up some chip dip.

Media technology has advanced to the point that things worth watching only make

economic sense when broadcast to millions, not to 80,000 or just a handful of

the rich.

The

greedy tycoon played by Michael Douglas had a two-pound, $3,995 Motorola phone

in the original "Wall Street" movie. Mobile phones for the elitehow 1987. Now

8-year-olds have cellphones to arrange play dates.

In

1991, a megabyte of memory was $50, amazing at the time. Given its memory,

today's 32-gigabyte smartphone would have cost $1 million back

then,

certainly an exclusive item for the wealthy. Heck, even 10 years ago, 32 gig cost 10

grand. But no one could build itvolume was needed to drive down

both cost and size and attract a few geeks to write some decent apps. So it

wasn't until there was a market for millions of smartphones that there was a

market at all. I just

bought a terabyte drive for $62 to rip all my Blu-Ray movies, and with Dolby 5.1

sound we all have private screening rooms

too.

Getty Images

True

enough, if you have $2.4 million or so in cash you can drive a Bugatti Veyron

Super Sport. But it's just fashion. Even a $16,500 Ford Focus can hit 80 on the

highway or get stuck in the same traffic as the rich person's ride. Plus, it

comes with what used to be expensive luxuries like side air bags, antilock

brakes, GPS guidance and voice-activated SYNC.

Yes,

the wealthy can strut around in more foo foo Jimmy Choos and Harry Winston

pendants, but so what?

That's all they've got left. Being envious of someone's nice outfit is no way to

go through life. Last I checked, envy is noted above gluttony on the

list of deadly sins. And by the way, I think Larry Page

drives a Prius, a different type of fashion.

Medical

care? Thanks to the market, you can afford a hip replacement and extracapsular

cataract extraction and a defibrillatorthe costs have all come down with

volume. Arthroscopic, endoscopic, laparoscopic, drug-eluting stentsthese are

all mainstream and engineered to get you up and around in days. They wouldn't

have been invented to service only the 1%.

I

admit that a private jet beats the TSA rub-a-dub. Along with his Prius, Larry Page has

a 767. But thanks to guys like Richard Branson and airline overbuild, you can

fly almost anywhere in the world for under $1,000. And most

places worth seeing are geared to a mass of visitors.

Spot

the pattern here? Just about every product or service

that makes our lives better requires a mass market or it's not economic to

bother offering. Those who invent and produce for the mass market get rich. And

the more these innovators better the rest of our lives, the richer they get but

the less they can differentiate themselves from the masses whose wants they

serve. It's the Pages and Bransons and Zuckerbergs who have made the unequal

equal: So, sure, income equality may widen, but consumption equality will become

more the norm.

To me,

being rich means covering the basic necessities, and then having a challenging

career, fun and fulfilling leisure time, and the love of family and friends.

Compared to 20 years ago, or even five years ago, chances are that you're

richer. Try to enjoy it.

Mr.

Kessler, a former hedge-fund manager, is the author most recently of "Eat

People: And Other Unapologetic Rules for Game-Changing Entrepreneurs"

(Portfolio, 2011).

December

29, 2011

In

October 2011, China set a new record for its exports to the United States, with

the value of its goods and services being imported into the U.S. reaching an

all-time high of $37.807

billion.

Unfortunately,

the year over year growth rate of China's exports to the U.S. indicates that the

U.S. economy, while doing a bit better than the months of May through September 2011, is still near recessionary

levels.

Worse,

we find that the year over year growth rate of U.S. exports to China has also

reached near-recessionary levels, even as the value of the goods and services

exported by the U.S. to China is still on track to peak by December 2011.

What

we suspect is that the respective growth rates of the trade between the two

nations are reaching a near-simultaneous inflection

point, where instead of growing, which we would expect if the economies

of China and the U.S. were both healthy, they are instead set to go flat or to

become negative, as both nations would appear to be now experiencing near

recessionary conditions.

It

would seem that not even the kind of massive

Keynesian economic stimulus spending that China engaged in back in 2009

and 2010 is sustainable for more than a couple of years, as all bubbles end.

It's only ever a question of when and how.

http://trueeconomics.blogspot.com/2011/12/28122011-ecb-new-evidence-on-public.html

Dr.

Constantin Gurdgiev

ECB

Working Paper 1406 (December 2011) titled "The

Public Sector Pay Gap in a Selection of Euro Area

Countries" looks at the relationship

between public and private sector wages over recent decades in the light of "the

increase in public sector employment in many countries, with relevant

implications for the overall macroeconomic performance and for public finances".

The study considered ten euro area countries: Austria, Belgium, France, Germany,

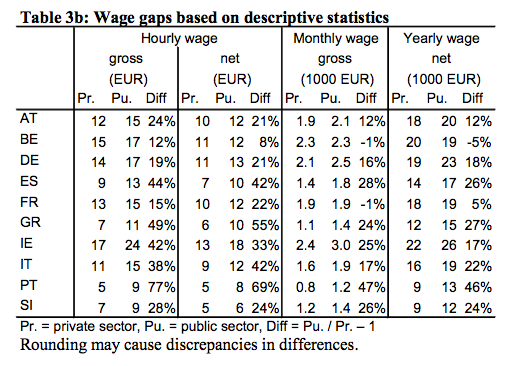

Greece, Ireland, Italy, Portugal, Slovenia and

Spain.

Per

authors: "According to national account aggregate data, the wage earned by a

representative public sector employee is higher than the one earned by a

representative private sector employee in all the countries of this study,

except Belgium, France and Germany. In particular, in the period 1995-2009 the

ratio of public to private compensation per employee is found to be consistently

below one in the case of France, slightly below one in the cases of Germany and

Belgium, around 1.1 for Austria, around 1.2-1.3 for Italy, Spain, Greece,

Ireland and Slovenia, and above 1.5 for Portugal."

"Available

data on union membership referring to the period 1997-2009 depending on the

country - show that union density (measured by the ratio

between reported membership and employed dependent labour force) is typically

much higher in the public than in the private sector (in the European countries

approximately twice as much). Among the countries included in

this study, union density rates are relatively high in Belgium (around 50%),

followed by Austria, Ireland, Italy and Portugal (in the 30- 40% range) and

Germany (27%); it is relatively low in France (about 8%) and Spain

(16%)."

The

summary of the premium evolution is provided here:

In

the chart above, Ireland has the second highest gap after

Portugal.

The

paper provides a reminder of a number of studies that have examined the

public-private sector wage gap in Ireland:

The

ECB research provides controls for a number of variables that can theoretically

explain diferences in pay between public and private sector, such as education

as skills proxy and gender, earnings groupings by percentiles, and

firm size. All are found to retain statistically signifcant public sector

earnings premium in the case of Ireland.

The

study also looks at one specific category - Education. "On average workers in

Education earn much higher wages with respect to workers with similar

characteristics in the private sector relative to workers in the other

sub-sectors, while workers in the Health sector are less at advantage, and as

in the case of Germany even at disadvantage with respect to their private sector

counterparts. This finding is confirmed on the basis of a formal statistical

test..."

And

the premium holds when controlling for workers' own

education:

So

overall, the study finds that: "A large body of literature has analysed the

issue using micro-data on single countries. Most of these studies find a

differential in favour of public sector workers, even after taking into account

some observable individual characteristics. As in the

previous studies, our results, referring to the period 2004-2007, point to a

conditional pay differential in favour of the public sector that is generally

higher for women, for workers at the bottom of the wage distribution, in the

Education and the Public administration sectors rather than in the Health

sector. We also find notable differences across countries, with Greece, Ireland, Italy, Portugal

and Spain exhibiting higher public sector premia than other

countries. The differential generally decreases when considering

monthly wages as opposed to hourly wages and if we restrict our comparison to

large private firms."

There

goes one of those "We are not Greece" comparatives that the Irish Government is

so keen on. When it comes to pay premium in the public sector, we are in the

Club Med (PIIGS) group after all.

What

will it take for markets to be convinced of the long-term soundness of European

public finances? Governments across the Continent are tightening their belts,

some with real cuts to services and entitlements, most with growth-killing tax

hikes.

Then

there is the wage bill. Though austerity has put a brake on salary increases,

holiday bonuses and new hiring, a working paper published this month by the

European Central Bank suggests governments have a long way to go to trim

civil-service pay down to size.

Economists

at eight European central banks studied public- and private-sector wages in 10

euro-zone countries in the period 1995-2009. In Europe as elsewhere, government

workers are on average older, better-educated and more likely to have managerial

roles than workers at private firms.

Yet

even controlling for these factors, the authors find that government

employees are paid much more than their counterparts in the rest of the

economy40%-70% more in net hourly wages in Greece, Italy, Portugal and Spain,

and a third more in Ireland. The gap is 20%-25% in Austria,

France, Germany and Slovenia. Belgium is a surprising outlier: In net hourly

wages, Belgian civil servants take home only 8% more than other workers and come

out slightly behind in yearly wages.

It's

difficult to compare these figures directly with ones for other developed

countries owing to differences in methodology and data, but signs suggest that

the pay differential on the Continent is particularly high. In the U.K., the public-private gap

in hourly wages is only 7.5% after controlling for education, age and

qualification, according to research by the

London-based

Institute for Fiscal Studies. The

authors of the ECB paper cite studies that suggest that the

U.S.

gap was 10%-15% during the 1970s but fell during the

1980s.

What

accounts for the Continent's wide public-private pay differential? It's not as

if European governments are employing fewer people, thereby justifying higher

pay. Among the 10

countries in the ECB sample, government share of the labor force ranges from 19%

in Germany to 38% in Belgium. In the U.S. government workers are 17% of nonfarm

payrolls.

A

better explanation is the power of government-employee unions and

special-interest groups in Europe. In countries where data are available, union

membership is twice as high among government workers than in the rest of the

labor force. Then

there is the entrenched character of government employment in Europe.

In many countries on

the Continent, civil servants enjoy total job security and a fixed schedule of

salary increases. Pay for civil servants also tends to be insulated from trends

in the private labor market.

Despite

all this, the public-private wage gap in Europe wasn't always so

large, and really began to widen after 1999.

That has at least

something to do with the introduction of the euro, which allowed employees to

compare their pay with peers in other countries. One result was that government

workers in particular were able to negotiate better

contracts. The currency union also reduced government

borrowing costs, but it failed to bring about reforms to contain public-sector

creep.

Recent

pay cuts for government employees have provoked rioting and protests in southern

Europe and the U.K. this year. That's one unhappy by-product of

large welfare states. They create powerful interest groups that make it hard to

take goodies back once they are given out. But the alternative is many more long

years of widespread doubt that Europe can borrow or grow its way back to

solvency.

Printed

in The Wall Street Journal, page 14

By

Richard W. Rahn

-

The

Washington Times

Monday,

December 26, 2011

Even

though some are predicting the end of the world in 2012, there is a possibility

it could turn out better than 2011 (a low bar). Many people who are not part of

the political class continue to advance civilization and make things better for

us - like the late Steve Jobs.

Dr.

Ito Briones, who is a biochemist research scientist, a medical doctor and

something of a Renaissance man, recently wrote to me that he thinks the greatest

discovery in medical science was the creation of iPS (induced pluripotent stem

cells, or stem cells from reprogrammed skin cells) by Drs. Shinya Yamanaka and

Kazutoshi Takahashi. According to Dr. Briones, "Even though the clinical

application of iPS cells remains untested, the theories about aging and stem

cells and the fountain of youth principles are groundbreaking and extremely

fascinating. IPS science continues to move very fast. ... The promise for cures

to cancer and other diseases appears plausible now with iPS science. What this

discovery has also done is to open scientists' minds to the concept that nothing

is indeed impossible in biology."

Other

potential good news is that not all members of the political class are

unprincipled, self-serving, ignorant and shortsighted. We are seeing a growing

band of smart, responsible and knowledgeable people being elected to Congress

and other political bodies. One example is Rep. Paul Ryan, Wisconsin Republican,

who is chairman of the House Budget Committee. Mr. Ryan, a fine economist, put

together an economically sound and politically realistic budget that passed the

House of Representatives but, not unexpectedly, died in the Democrat-controlled

Senate. There is a real possibility that a sufficient number of the American

people will be rational enough to elect new members to the House and Senate (and

the presidency) to pass a Ryan-type budget before the United States goes off the

fiscal cliff, like Greece.

In

democratic countries, many politicians get themselves elected by making promises

for spending programs that the citizens cannot or are unwilling to pay

for. The

result is persistent deficit spending that ultimately spirals out of control.

The good news is that some democratic countries have learned how to avoid the

spending/deficit trap, and those countries can serve as examples for the less

prudent majority. (See accompanying chart.)

The

best example is Switzerland. The Swiss have managed to be fiscally responsible

for many decades, in part because they have a highly decentralized, direct

democracy. Most governmental functions take place at the local level rather than

the federal level in Switzerland, and as a result, the local governments must

compete with each other on taxes, regulations, etc., which tends to hold down

the growth in government and promotes liberty. Where government is close to the

people, and where the democratic process is direct, the people can more directly

hold elected officials responsible for misspending and

mismanagement.

The

United States was designed by its founders to have a small and relatively weak

central government, in which most of the government functions and power were

supposed to be at the state and local level.

The 10th Amendment to

the U.S. Constitution is very explicit: "The powers not

delegated to the United States by the Constitution nor prohibited by it to the

States, are reserved to the States respectively or to the people." The potential

good news is that as a result of the presidential debates, more people are

becoming aware of the 10th Amendment and are beginning to understand that if

Congress and the courts stopped ignoring this amendment, the U.S. likely would

have a smaller, more effective and more fiscally sound

government.

Sweden

and Canada provide role models for how highly developed democracies that have

created unsustainable welfare states can find peaceful and constructive ways out

of the dilemma. In

the mid-1990s, both countries were stagnating and headed toward a Greek-style

credit default because of the drag of bloated government spending, taxing and

regulation. In both

countries, the parties of the left and right came together to reverse course by

reducing tax rates, spending and destructive regulation and privatizing much of

what had been nationalized. Real growth has been revived in both Canada and

Sweden, and they both have very manageable debt-to-gross-domestic-product

ratios. Because Sweden is a small, homogenous country, it is

able to maintain a larger government as a percentage of GDP and still obtain

normal rates of economic growth than can more heterogeneous countries like the

U.S. and Switzerland.

The

good news is that it is well-known what economic reforms are necessary to revive

growth and fiscal sanity in the major European countries and

America. But

it also takes leaders who can explain what needs to be done and persuade the

people to endure the pain of the necessary transitional hardship in the way

British Prime Minister Margaret Thatcher and President Reagan

did.

As a

reality check on the potential good news, my friend Jim Stewart, a neurologist,

asked: "While the medical community is indeed making great strides in extending

our lives, who ... wants to live longer if the politicians keep making things

worse?"

Richard

W. Rahn is a senior fellow at the Cato Institute and chairman of the Institute

for Global Economic Growth.

2011-12-23

13:28:19

http://www.ocregister.com/common/printer/view.php?db=ocregister&id=332895

Our

lesson for today comes from the Gospel according to Luke. No, no, not the

manger, the shepherds, the wise men, any of that stuff, but the other

birth:

"But

the angel said unto him, Fear not, Zacharias: for thy prayer is heard; and thy

wife Elisabeth shall bear thee a son, and thou shalt call his name

John."

That

bit of the Christmas story doesn't get a lot of attention, but it's in there

Luke 1:13, part of what he'd have called the back story, if he'd been a

Hollywood screenwriter rather than a physician. Of the four gospels, only two

bother with the tale of Christ's birth, and only Luke begins with the tale of

two pregnancies. Zacharias is surprised by his impending paternity "for I am

an old man and my wife well stricken in years." Nonetheless, an aged, barren

woman conceives and, in the sixth month of Elisabeth's pregnancy, the angel

visits her cousin Mary and tells her that she, too, will conceive. If you read

Luke, the virgin birth seems a logical extension of the earlier miracle the

pregnancy of an elderly lady. The physician-author had no difficulty accepting

both. For Matthew, Jesus' birth is the miracle; Luke leaves you with the

impression that all birth all life is to a degree miraculous and

God-given.

POLITICAL

CARTOONS:

75

cartoons and photos of Korean leader Kim Jong-Ill and

sons

We now

live in Elisabeth's world not just because technology has caught up with the

deity and enabled women in their fifties and sixties to become mothers, but in a

more basic sense. The problem with the advanced West is not that it's broke but

that it's old and barren. Which explains why it's broke. Take Greece, which has

now become the most convenient shorthand for sovereign insolvency "America's

heading for the same fate as Greece if we don't change course," etc. So Greece

has a spending problem, a revenue problem, something along those lines, right?

At a superficial level, yes. But the underlying issue is more primal: It has one

of the lowest fertility rates on the planet. In Greece, 100 grandparents have 42

grandchildren i.e., the family tree is upside down. In a social democratic

state where workers in "hazardous" professions (such as, er, hairdressing)

retire at 50, there aren't enough young people around to pay for your

three-decade retirement. And there are unlikely ever to be

again.

Look

at it another way: Banks are a mechanism by which old people with capital lend

to young people with energy and ideas. The Western world has now inverted the

concept. If 100 geezers run up a bazillion dollars' worth of debt, is it likely

that 42 youngsters will ever be able to pay it off? As Angela Merkel pointed out

in 2009, for Germany an Obama-sized stimulus was out of the question simply

because its foreign creditors know there are not enough young Germans around

ever to repay it. The

Continent's economic "powerhouse" has the highest proportion of childless women

in Europe: one in three fräulein have checked out of the motherhood

business entirely. "Germany's working-age population is likely to decrease 30

percent over the next few decades," says Steffen Kröhnert of the Berlin

Institute for Population Development. "Rural areas will see a massive population

decline, and some villages will simply

disappear."

If the

problem with socialism is, as Mrs. Thatcher says, that eventually you run out of

other people's money, much of the West has advanced to the next stage: it's run

out of other people, period. Greece is a land of ever-fewer customers and fewer

workers but ever more retirees and more government. How do you grow your economy

in an ever-shrinking market? The developed world, like Elisabeth, is barren.

Collectively barren, I hasten to add. Individually, it's made up of millions of

fertile women, who voluntarily opt for no children at all or one designer kid at

39. In Italy, the home

of the Church, the birthrate's somewhere around 1.2, 1.3 children per couple

or about half "replacement rate." Japan, Germany and Russia are already in net

population decline. Fifty percent of Japanese women born in the Seventies are

childless. Between 1990 and 2000, the percentage of Spanish women childless at

the age of 30 almost doubled, from just over 30 percent to just shy of 60

percent. In Sweden, Finland, Austria, Switzerland, the Netherlands and the

United Kingdom, 20 percent of 40-year old women are childless. In a recent poll,

invited to state the "ideal" number of children, 16.6 percent of Germans

answered "None." We are living in Zacharias and Elisabeth's world by

choice.

America

is not in as perilous a situation as Europe yet. But its rendezvous with

fiscal apocalypse also has demographic roots: The baby boomers did not have

enough children to maintain the solvency of mid-20th century welfare systems

premised on mid-20th century birthrates. The "Me Decade" turned into a Me

Quarter-Century, and beyond. The "me"s are all getting a bit long in the tooth,

but they never figured there might come a time when they'd need a few more

"thems" still paying into the treasury.

The

notion of life as a self-growth experience is more radical than it

sounds. For most of

human history, functioning societies have honored the long run: It's why

millions of people have children, build houses, plant trees, start businesses,

make wills, put up beautiful churches in ordinary villages, fight and, if

necessary, die for your country. A nation, a society, a community is a compact

between past, present and future, in which the citizens, in Tom Wolfe's words at

the dawn of the "Me Decade," "conceive of themselves, however unconsciously, as

part of a great biological stream."

Much

of the developed world climbed out of the stream. You don't need to make

material sacrifices: The state takes care of all that. You don't need to have

children. And you certainly don't need to die for king and country. But a

society that has nothing to die for has nothing to live for: It's no longer a

stream, but a stagnant pool.

If you

believe in God, the utilitarian argument for religion will seem insufficient and

reductive: "These are useful narratives we tell ourselves," as I once heard a

wimpy Congregational pastor explain her position on the Bible. But, if

Christianity is merely a "useful" story, it's a perfectly constructed one,

beginning with the decision to establish Christ's divinity in the miracle of His

birth. The hyper-rationalists ought at least to be able to understand that

post-Christian "rationalism" has delivered much of Christendom to an utterly

irrational business model: a pyramid scheme built on an upside-down pyramid.

Luke, a man of faith and a man of science, could have seen where that leads.

Like the song says, Merry Christmas, baby.

©MARK

STEYN

Timothy Taylor has a must-read post.

(I could say that almost every day, but today I am going to provide additional

commentary.) It's long, but here is a brief excerpt.

In fact,

Megan McArdle reminds us that we tax

the poor at high marginal rates by phasing out benefits at low levels of

income.

http://conversableeconomist.blogspot.com/2011/12/government-redistribution-international.html

Income

inequality has been growing in most high-income countries around the

world.

How much do the redistribution policies of government hold down this growth in

inequality? The OECD has published Divided

We Stand: Why Inequality Keeps Rising. (The report can be read for free

on-line with a slightly clunky browser, and a PDF of an "Overview" chapter can

be downloaded.) Chapter 7 of the report discusses "Changes in Redistribution in

OECD Countries Over Two Decades," which basically means from the mid-1980s to

the mid-2000s. The chapter draws on a longer background paper that is freely

available on-line: Herwig Immervoll and Linda Richardson's paper, "Redistribution

Policy and Inequality Reduction in OECD Countries: What Has Changed in Two

Decades?"

The United States does relatively

little redistribution in comparison with other OECD countries.

This graph from the "Overview" of the OECD report compares the inequality of

market incomes to the inequality of disposable income after taxes and benefit

payments. Inequality is

measured by a Gini coefficient. For a more detailed explanation of how this is

measured, see my November 1 post on Lorenz curves and Gini

coefficients. But as a quick overview, it suffices

to know that a Gini coefficient measures inequality on a scale from zero to 1,

where zero is perfect equality where everyone has exactly the same income and 1

is perfect inequality where one person has all the income. The

United States has one of the most unequal distributions of market income and of

disposable income, and in this comparison group, U.S. policy does relatively

little to reduce the disparity. The OECD writes: "Public cash

transfers, as well as income taxes and social security contributions, played a

major role in all OECD countries in reducing market-income inequality. Together,

they

were estimated to reduce inequality

among the working-age population (measured by the Gini coefficient) by an

average of about one-quarter across OECD countries. This redistributive effect

was larger in the Nordic countries, Belgium and Germany, but well below average

in Chile, Iceland, Korea, Switzerland and the United States (Figure

9).

Any

economy that has a progressive tax code and benefits for those with low incomes

will find that as inequality increases, redistribution will also increase

automatically as a result of these preexisting policies Some countries may also

take additional steps, when faced with rising inequality of market incomes, to

raise the amount of redistribution. A table in Ch. 7 of the OECD report

calculates how much of the increase in increase in market incomes from the

mid-1980s to the mid-2000s was offset by a rise in

redistribution.

Denmark is the extreme case:

increased redistribution from the mid-1980s to the mid-2000s offset more than

100% of the rise in inequality of market incomes. In a number of countries, the

rise in redistribution offset from 35-55% of the rise in inequality of market